The iron ore and steel industry accounts for approximately 5% of total global CO2 emissions. On average, 1.9 tonnes of CO2 are emitted for every tonne of steel produced so the challenge is on for green steel technology to decrease emissions and decrease costs. The change to a low emissions is challenging and the following components include.

- Mining

- Shipping

- Change heat supply from fossil fuel to green H2 or renewable energy

- Change from blast furnace to direct reduction

Stranded Asset Risk

The steel industry could face $US518 billion in stranded asset risk as countries work towards meeting their long-term carbon neutrality commitments, if the 345.3 million tonnes per annum (mtpa) of emissions-heavy blast furnace basic oxygen furnace capacity (BF-BOF) proposed or under construction is fully developed, according to new data from Global Energy Monitor’s Global Steel Plant Tracker. Transitioning to less carbon-intensive steelmaking is a big part of countries meeting their net zero goals. (Global Monitor 2022)

Reduction in Emissions Will Be A Combination

- Renewable energy is cheaper power than fossil power..

- Mining. CSIRO estimated GHG emissions were 11.9 kg CO2e for mining and processing 1 t of iron ore. The embodied energy values were 153 MJ/t ore for iron ore. Results showed that loading and hauling made the largest contributions (approximately 50%) to the total GHG emissions from the mining and processing of iron ore.

- H2 may replace methane gas and depending on changes in H2 production

- Customers will demand green steel

- Two or 3 new technologies may replace blast furnaces. (DRI or direct reduction iron)

Comparison of Blast Furnace and Hydrogen Direct Reduction

Data from Carbon Commentary The extra costs of decarbonised steel 2020″

| Item of Cost | Blast Furnance Energy | Blast Furnace Cost | Hydrogen Direct Reduction energy | Hydrogen Direct Reduction cost |

|---|---|---|---|---|

| Oil | 81kWh | €4 8 litres of oil at a price of around $0.5/litre | ||

| Coal | 5,510 kWh | €96 Coking coal of 24 MJ/kg at $130/tonne, $1.10=1€ | ||

| Graphite | 45kWh | €6 small flakes, $550 a tonne, energy value 32.8 MJ/kg | ||

| Biomass Fuel | 560 kWh | €5 Same price as low carbon content coal | ||

| Electricity (NordPool price of €45/MWh) | 235kWh | $11 | 3,488 kWh | €157 |

| Total Cost | 5,826kWh | €111 | 4,093kWh | €168 |

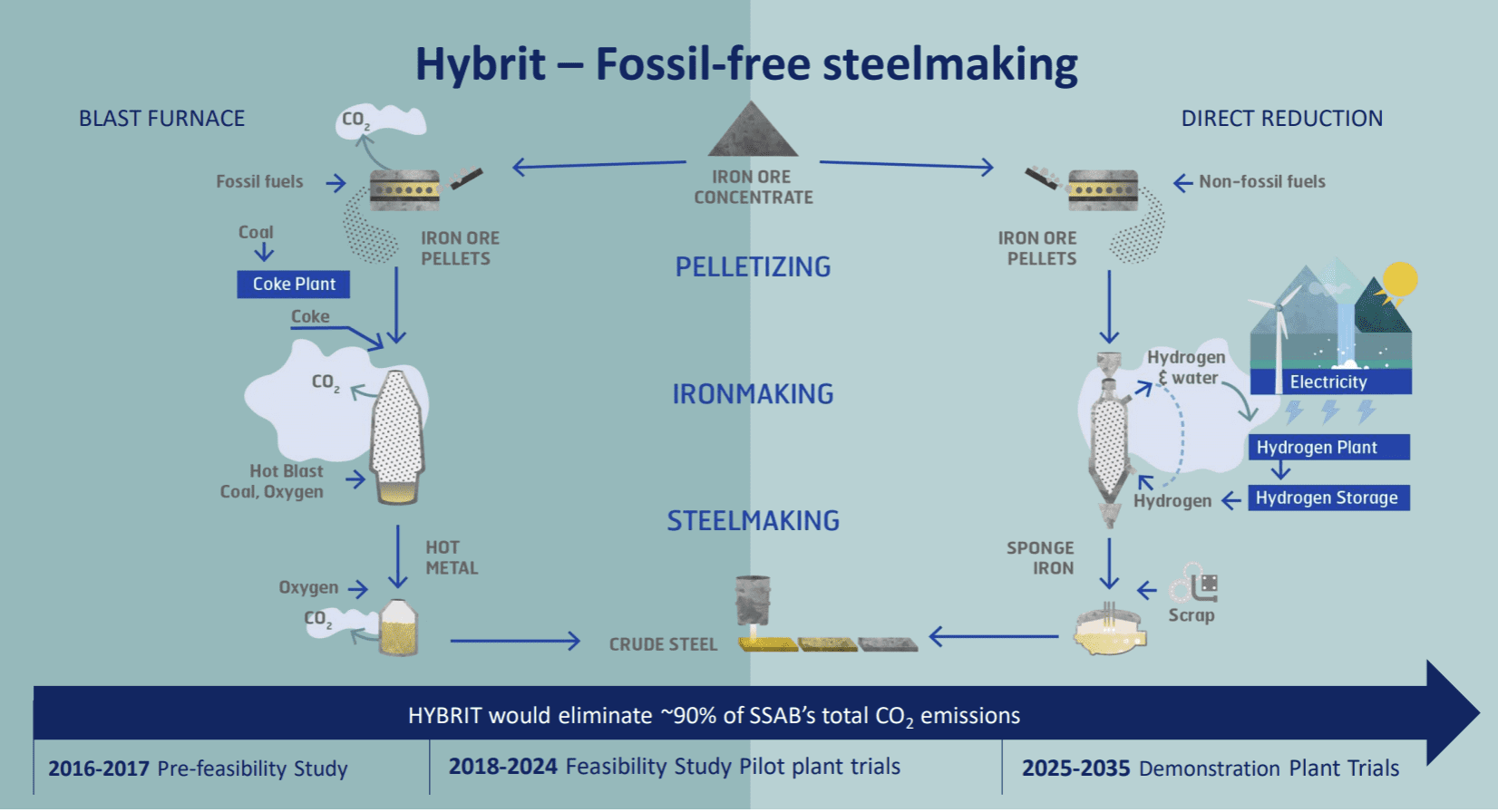

SSAB has a plan to have full commercial deliveries of green steel by 2026. The quality and properties of fossil-free steel will be the same as SSABs steel of today. The steelmaking, rolling and heat treatment processes determine the steel properties. The objective is to remain the same. The only difference in the process is that the energy used will renewable and not fossil fuel-based. The 2 areas are the creation of the iron ore pellets, and the second is ironmaking.

Capital Cost of Changing to DRI

There is a change in equipment as well. Capturing the oxygen in the iron ore to produce steel is not the sole issue. A steelmaker switching to hydrogen will require new capacity in the form of direct reduction furnaces, and possibly new electric arc furnaces as well.

How expensive will this equipment be? German steel maker ThyssenKrupp estimates total expected cost is ~ €10bn for its 13 million tonnes of steel production. This implies a figure of about €770m capital investment per million tonnes of steel, or around €1 trillion over the course of the entire transition. SSAB in Sweden and Finland makes about 6m tonnes currently in new steel each year, implying a total conversion cost of about €4.6 billion, spread over 25 years to 2045, or about €185m a year.

Green hydrogen is too expensive to use in our EU steel mills, even though we’ve secured billions in subsidies’

Geert van Poelvoorde, head of ArcelorMittal’s European operations Hydrogen Insight 2024

Instead, the Luxembourg-based steelmaker appears to be intending to use fossil gas instead of H2 indefinitely in its proposed “green steel” plants — or it may even delay the construction of subsidised “direct-reduced iron” (DRI) manufacturing units in Europe in favour of importing green hydrogen-derived DRI from abroad

Top 10 Miners – And Who is focused on Green Steel

Mining.com lists the world’s top 20 biggest iron ore operations

The top 5 miners (BHP, Vale, FMG, Rio, Arcelormitta) dig up iron ore which is about 60% iron ore, cart all of it to port, ship to China or India, ship coal there as well and then ship the steel globally. The energy and cost of shipping and transport costs are also huge.

Mining and processing hematite and magnetite ores

High-grade hematite ore is referred to as direct shipping ore (DSO) as, once mined, the ore goes through a simple crushing and screening process before being exported for steel-making. Australia’s hematite DSO from the Hamersley province averages from 56% to 62% Fe.

Like hematite ores, magnetite ores require initial crushing and screening but also undergo a second stage of processing using the magnetic properties of the ore to produce a concentrate. Further processing of magnetite involves agglomeration and thermal treatment of the concentrate to produce pellets. These can Blast furnaces or direct reduction steel-making plants will use the pellets. Pellets contain 65% to 70% Fe, a higher grade compared to the hematite DSO currently exported from the Hamersley province. Additionally, when compared to hematite DSO, the magnetite pellets contain lower levels of impurities, such as phosphorous, sulphur and aluminium. Thus, magnetite pellets are a premium product and attract higher prices from steel makers. This offsets the lower ore grades and higher costs of production

Other Green Steel Technologies

Recently, Boston Metal, a startup in the USA have focused on Molten Oxide Electrolysis which uses electricity to turn iron ore into liquefied metal. Boston Metal claims it is the most efficient way of producing steel without carbon emissions, and the company plans to be producing a commercial quantity of green steel using this process from 2025. They are already producing liquid ion. Can they scale fast enough. They have the investors, including BHP/ Vale / BMW.

In their MOE cell, an inert metallic anode is immersed in an iron ore electrolyte. The clean, high purity liquid metal can be sent directly to ladle metallurgy — no reheating required.

Comprehensive View from Stockhead

Steel blast furnaces use hard coking coal as a reducing agent to strip oxygen from iron ore to make crude steel. This process, responsible for 90% of output in the world’s largest and only billion-tonne-a-year steel market China, generates around 2t of CO2 for every tonne of steel. Cleaner processes like direct reduced iron and electric arc furnace, the latter of which primarily uses scrap steel, burn far less fossil fuel, generating around 1.4 and 0.4t of CO2 per tonne of steel currently. DRI, powered by gas, could become even greener in the future with the introduction of ‘green hydrogen’ as a replacement for natural gas. But both have limitations.

Check out this report from Stockhead in Mid 2022. there are 4 issues

- Source and type of iron ore

- Energy source – metallurgic coal versus gas versus hydrogen

- Electricity for mining and processes

- DRI-SAF technology

Thyssenkrupp is planning to replace four of its blast furnaces with DRI-SAF plants by 2045, starting with the first two in 2025 and 2030. Key issues includel

- Proving up the process with melting stage to use 65% Fe or less blast furnace grade pellets in the DRI process.

- Reduce CO2 emissions by 30% by 2030

- Producing 400,000t of green steel by 2025

- Produce 3Mt by 2030.

- Start with gas for its first 1.2Mt DRI plant

- Shift shift to hydrogen if and when that becomes commercially viable.

- The first plant goes to FID in 2023.

Iron Ore Purity and Source for DRI

DRI in particular requires a high grade, low impurity iron ore above 66% (4% above the benchmark index and 5-6% above the grades of major Pilbara iron ore producers) to function. Only about 4% of iron ore globally is this purity.

More Reading

- Green hydrogen is too expensive to use in our EU steel mills, even though we’ve secured billions in subsidies. Hydrogen Insight 2024 https://www.hydrogeninsight.com/industrial/green-hydrogen-is-too-expensive-to-use-in-our-eu-steel-mills-even-though-weve-secured-billions-in-subsidies/2-1-1601199