Some big insurance companies see that infrastructure globally is becoming uninsurable due to climate change. From Paul Dickinson podcast 220 of Outrage and Optimism. A key concern of non USA reinsurers is a Trump presidency would pull back on climate change policies and investment.

His story is that in 2001, he asked the head of general insurance at the Association of British Insurers – “has anything like climate change happened before”? The response was that after the Nazi bombing of Guernica (1937), the world’s insurance companies got together in 1938. They decided insurance won’t cover property damage due to war. The renewable notices in 1939 and 1940 reiterated the pullback. Going bust is not an issue, as insurance companies increase policy fees or no longer insure.

Rising Insurance

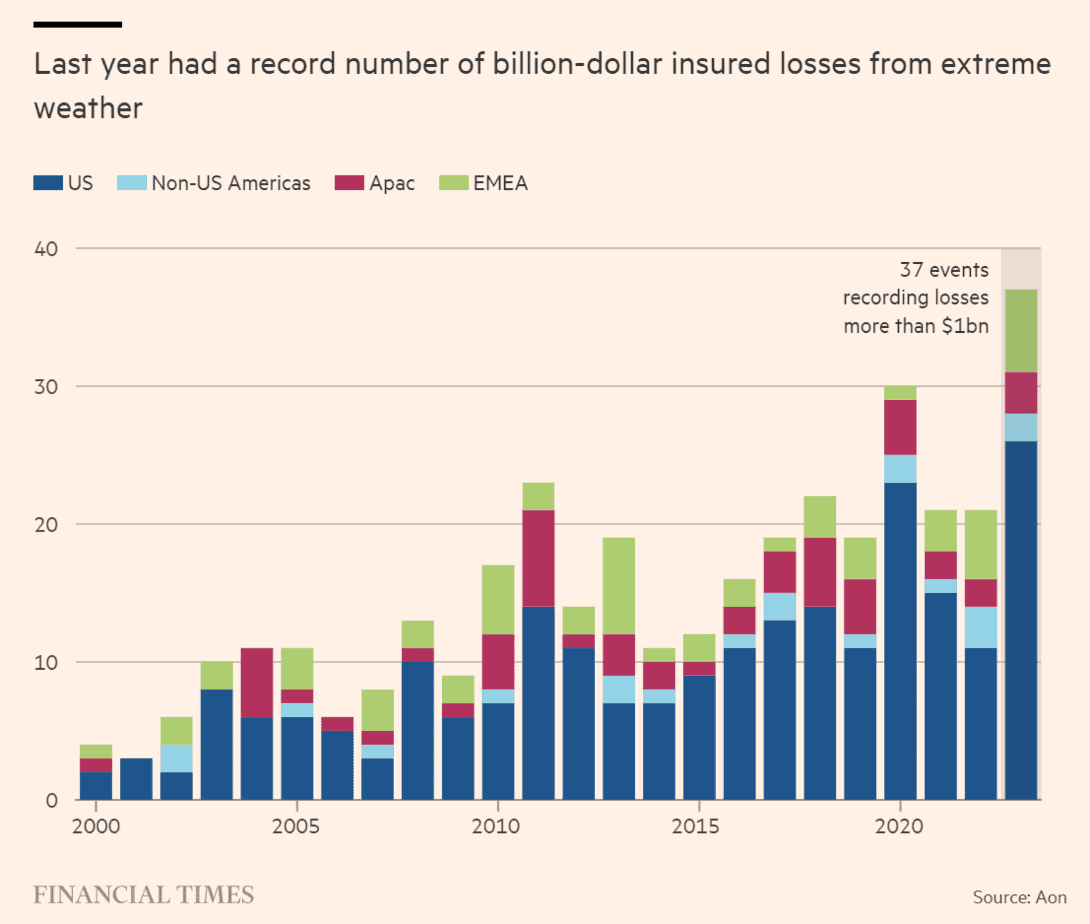

“Four consecutive years when insurance losses from natural catastrophes topped $100b, previously the mark of a remarkably bad year, has spooked executives”, – as rising premiums become a de facto carbon price on consumers.

Signs of Becoming Uninsurable due to Climate Change

Australia

One in 25 Australian properties will be effectively uninsurable by 2030, due to rising risks of extreme weather and climate change, a detailed analysis from the Climate Council has found. A digital map developed shows uninsurable prices.

USA

About 35.6 million properties — one-quarter of all U.S. real estate — face increasing insurance prices and reduced coverage due to high climate risks.

Hurricanes and flooding cause significant damage to several regions of the United States each year. The National Centers for Environmental Information compiles data on the most expensive weather and climate disasters, and according to their research, hurricanes were responsible for the majority of expenses. 60 particularly strong storms in 2022 each resulted in an average of $22.2 billion in damages. Flooding was fourth on the list, causing an average of $4.8 billion in damage for each event. The top five areas where housing is uninsurable in the USA (article) include

- Floridas Gulf Coast

- Houston’s Addicks and Barker Reservoirs

- Hull, Massachusetts faces annual rate increases of 20% a year due to flooding

- San Rafael canal areas. Flood insurance rates in San Rafael are among the highest in the state, costing at least $1,800.

- Montpelier and the other towns that border the Winooski River are at a significantly higher flood risk than some other areas. Because of this, the average cost of flood insurance in Montpelier is $2,400, nearly $800 more than the average for the state.

- Montpelier, Vermont, and the other towns that border the Winooski River are at a significantly higher flood risk than some other areas. The average cost of flood insurance in Montpelier is $2,400, nearly $800 more than the average for the state.

Wildfires are worse. Increasingly insurers withdraw coverage, leaving millions of individuals and even entire communities vulnerable. Some California locations and towns are uninsurable – CBS https://www.cbsnews.com/news/insurance-policy-california-florida-uninsurable-climate-change-first-street/

Economic Impact of Storms

More Reading

- Financial Times: The uninsurable world: what climate change is costing homeowners (FT Big Read)